.svg)

Q2 2026 Commercial Mortgage Market Update

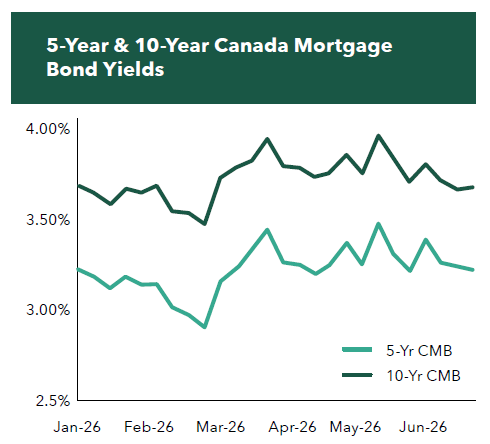

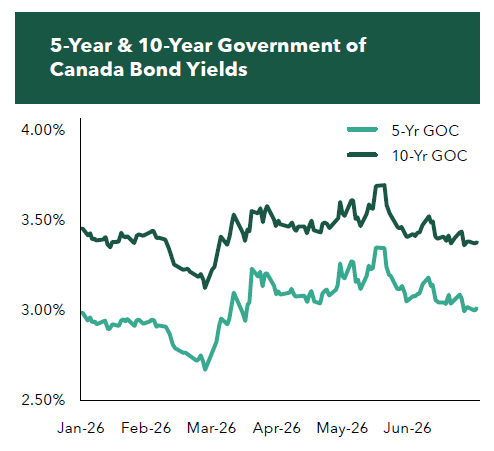

The second quarter gave us a market learning to live with an unresolved backdrop rather than reacting to a fresh shock. The Bank of Canada held the overnight rate at 2.25% through April and June, its fifth consecutive hold, caught between a soft domestic economy on one side and an energy-driven inflation scare tied to the ongoing conflict in the Middle East on the other. Bond yields, which spiked sharply earlier in the year, spent most of Q2 grinding back down as evidence accumulated that higher energy prices were not feeding broadly into the rest of the price basket. By late June, the 10-year Government of Canada yield eased below 3.40%, its lowest level in over three months, and the 5-year was holding in the 3.00% range. The takeaway for borrowers heading into Q3 is a market that has stopped bracing for the worst case, without getting the clean rate relief many had hoped for at the start of the year.

Market Overview

Conditions across most commercial asset classes remained stable through Q2, extending the pattern we have been describing for several quarters now. Lenders continue to compete hardest for high-quality industrial, necessity-based retail, and conventional multi-family properties, and spreads for best-in-class assets with credible sponsors and in-place income stayed tight. On lower-leverage financing for top-tier properties, that competition has pushed spreads into the low 120s over benchmark, and we have seen a handful of deals price at 120 flat, a level of aggression on the highest-quality end of the market that we have not seen in some time. Banks have remained active originators, and their pricing on strong deals continues to sit as competitive as, or tighter than, their life insurance company competitors.

Commercial construction financing is also seeing a genuine pickup in appetite. Multiple bank and pension lenders are now aggressively in the market for construction deals, competing on both leverage and pricing rather than simply defending existing relationships, a meaningful shift from the more defensive construction lending posture we described through most of last year.

CMHC Policy Changes

The shift back toward CMHC-insured construction financing that we flagged last quarter has only gained momentum. CMHC added a new wrinkle in Q2, raising the operating expense benchmarks used in MLI Select underwriting effective June 8, 2026. As with most CMHC benchmark changes, the announcement triggered a scramble to get applications filed under the prior, more favorable benchmarks before the deadline, adding to an already busy queue heading into the September 30 energy efficiency transition deadline. We expect the CMHC queue to significantly increase as applications start pouring in to beat the September deadline once again.

Other CMHC policy changes were geared towards lender monitoring and compliance, especially with MLI Select affordability and energy efficiency measures for completed buildings. Expect increased review of energy efficiency reports on submission and verification of leases upon lease-up.

Presale Condo Market: Governments Step In to Move Inventory

The defining development this quarter was not a shift in buyer appetite but direct government intervention in the unsold inventory overhang, in both Vancouver and the GTA.

In Vancouver, Prime Minister Mark Carney and Premier David Eby announced a federal-B.C. partnership under which Build Canada Homes and BC Housing will use “innovative financing tools” to acquire and convert more than 2,200 completed, unsold condo units into rent-to-own affordable housing, with a total potential spend in the range of $1.45 billion (the federal government’s share pegged at roughly 10%, or about $145 million). CMHC data cited in the announcement showed 4,376 completed condos sitting empty across Metro Vancouver as of May, up 76% year over year. The reaction has been sharply divided. Officials insist the program will only buy units at a discount to construction cost and won’t bail out developers at the top of the market, while critics, including federal Conservative leader Pierre Poilievre, have called it a taxpayer-funded bailout for developers and lenders who made poor bets on the boom.

Ontario has been running a similar playbook, just earlier and with a private-sector lead. The Building Ontario Fund committed up to $300 million in mezzanine debt and a nominal equity stake to anchor High Art Capital’s $1.3 billion GTA Rental and Affordable Housing Initiative, which is acquiring blocks of newly completed, unsold condo units in Toronto and the surrounding regions and converting them into long-term rentals, with roughly 550 of the targeted 2,200 units earmarked as below-market affordable housing. It has drawn some of the same bailout criticism as the B.C. program, though the structure, private capital paired with a public mezzanine loan rather than a direct government purchase, has been positioned as less politically exposed.

For our purposes, the practical read is this: both programs are a symptom of the same underlying problem, a historic overhang of completed, unsold condo inventory in both major markets that the private market has not been able to absorb on its own. Whether or not these programs move the needle at scale, they are a clear signal that governments now view the unsold inventory problem as systemic rather than transitory, which should factor into how lenders and sponsors think about exit assumptions on anything still in the pipeline.

Beyond the two headline programs, conditions in the broader presale market are largely unchanged from last quarter. New launches remain scarce, financing for inventory and presale-secured construction still carries hard presale thresholds and longer interest reserves than the market considered standard two years ago, and closing risk remains a defining credit concern rather than a secondary one.

Not surprisingly, with this much unsold inventory in the market, condo construction financing remains challenging as does residential land financing, even with solid municipal approvals and density in place. Lenders are simply not taking the risk unless construction financing (and presales) are in hand.

Land Financing

While many borrowers are in the market seeking to refinance land, only a small percentage of opportunities that cross our desk ultimately get financed. When clients ask what separates financeable transactions from those that are not, we point to three key criteria:

1. Supportable land value - The ascribed land value must be reasonable and supported by a residual land value analysis based on a current rental pro forma and construction budget.

2. A defined path to development - The project must have a clear and credible timeline for rezoning and ultimately construction, generally no longer than 3 years.

3. A viable construction takeout - The borrower must have the equity required to trigger construction financing, along with evidence that they can qualify for the construction loan upfront.

In the previous market cycle, many land loans were underwritten on the assumption that the remaining pieces would eventually fall into place. In many cases, they did not. Today, lenders need confidence that the land value is supportable, the exit strategy is clearly defined, and the sponsor has both the financial capacity and execution capabilities to deliver the project.

Conclusion

While market friction remains, the silver lining is that transactions are still getting done. Although financing timelines have lengthened and lender underwriting remains disciplined, capital continues to be available for well thought out and well-structured opportunities. Borrowers with realistic expectations, a clear business plan, and a defined path to execution continue to attract capital while transactions dependent on aggressive valuations or future market improvements remain challenging. As we move into the second half of 2026, we expect liquidity to remain strongest for stabilized assets and purpose-built rental developments, while construction, land, and condominium financing will continue to require greater selectivity and discipline.

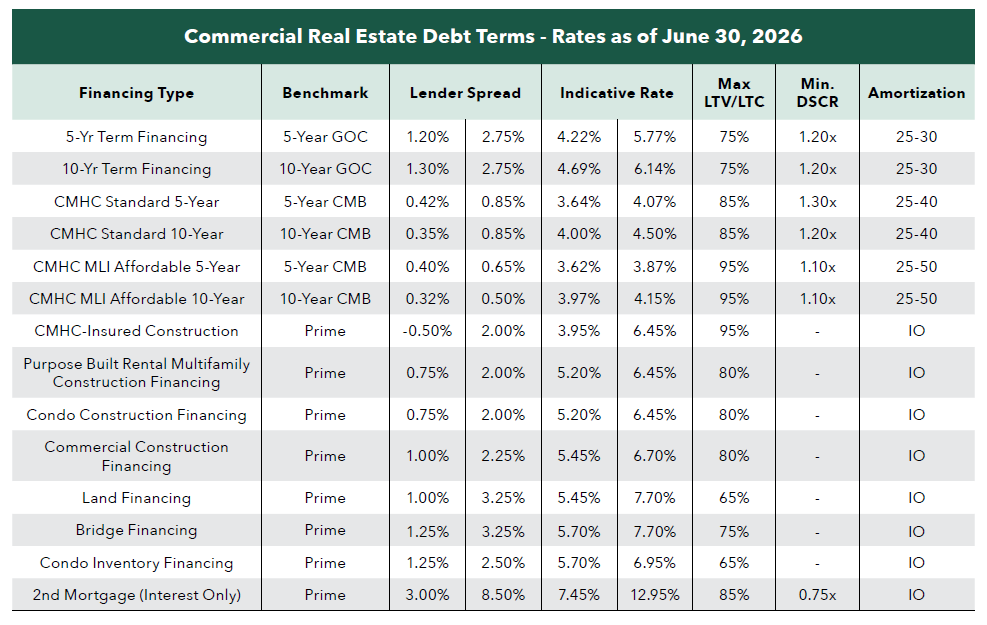

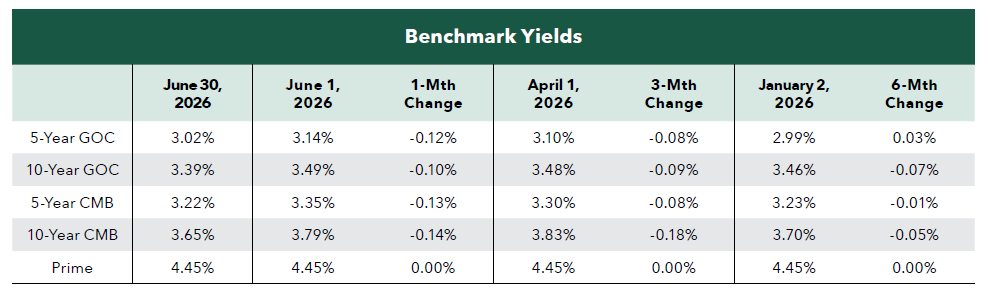

Selected Commercial Debt Terms and Benchmark Yields

Sign up for our newsletter

.svg)

.svg)