.svg)

Q1 2026 Commercial Mortgage Market Update

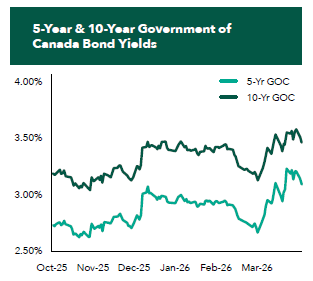

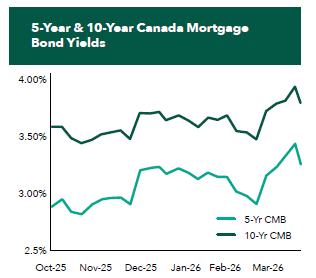

Just when it looked like the commercial real estate financing market was finding its footing, Q1 2026 introduced a new variable that few had penciled in. The Iran conflict, which escalated in late February, sent oil prices sharply higher and reignited inflation concerns that central banks had spent the better part of two years trying to put behind them. Bond yields moved quickly, and borrowers who had been patiently waiting for a more constructive fixed rate environment found themselves re-running numbers on deals that had made sense only weeks earlier. The Bank of Canada held rates steady through the quarter. The transmission is straightforward: higher oil feeds into energy costs, energy costs feed into CPI, and bond investors demand more yield to hold duration when the inflation outlook gets murkier. The Bank of Canada held, but the bond market did not wait for permission to move.

Demand For Income Producing Properties Increasing

Conditions in the commercial mortgage market were broadly unchanged from last quarter across most asset classes. Lenders continued to compete for high-quality industrial, necessity-based retail, and conventional multifamily, with pricing remaining attractive for best-in-class assets. The story on spreads is largely the same one we have been telling for several quarters now: strong assets with in-place income and credible sponsors receive the most competitive terms. Banks are actively back in the market originating and their spreads are becoming as tight or tighter than their life insurance competitors.

Office continued its tentative recovery. It is not a full reopening of the credit window, but more lenders are writing term sheets for well-leased Class A product in core markets than were doing so a year ago. The selectivity is still high, but the conversation has changed. Where the Iran conflict and the resulting bond volatility showed up most clearly was in execution timelines. Lenders who were open for business in January were re-running their numbers by March. Deals that penciled at the start of the quarter needed to be re-underwritten by the end of it. The borrowers who fared best were those who had locked rate early or built in enough cushion to absorb a move.

CMHC Construction: Back to Insured

The pendulum has swung back toward CMHC for purpose-built rental construction financing, and the energy efficiency changes are a meaningful part of that story.

The conventional construction to CMHC takeout structure served developers well over the past several quarters. Speed of funding, quicker access to the ground, and the potential for a higher takeout on refinancing if rent growth materialized were all compelling reasons to avoid the front-end insured approval process. That strategy is shifting. With rents declining across Canada, and particularly in the GTA, the rent growth thesis that underpinned some of those conventional underwriting models has been quietly set aside. No lender is modeling rent growth today. CMHC is adjusting its market rents in real time, and borrowers going the insured route benefit from higher up-front leverage without needing to project a recovery that the market is not signaling.

The other driver pushing files back to CMHC is the energy efficiency update, which will come into effect in September of this year. Developers who cannot redesign their buildings to meet NECB 2020 standards, or the higher energy efficiency threshold required to score meaningful MLI Select points under the new framework, are finding that CMHC’s insured program still offers a better outcome than conventional alternatives, even with the added complexity. Those who submit files ahead of the September change will be locked in under the prior NECB 2017 framework.

On queue times, the improvement we observed in late 2025 has held. Straightforward refinancings and purchases for sub-25-unit properties are beginning to receive Certificates of Insurance in a matter of weeks (some as fast as a week). The trade-off remains the same: CMHC is applying more thorough quality assurance, with deeper scrutiny on complex files such as construction, complex sponsor profiles, and any commercial components to the projects. Affordability-weighted applications continue to receive preferential treatment. If your file has complexity in any of those areas, build the timeline accordingly. As always with a looming CMHC deadline, we anticipate the CMHC queue to yet again build closer to the September deadline. Developers, get your applications in now.

Pre-Sale Market: Non-Existent

It would be generous to call the pre-sale market quiet. New launches are effectively non-existent this quarter, and lenders have followed suit. The few who remain active in the space are requiring hard presale thresholds that are difficult to achieve in the current environment, alongside more equity and longer interest reserves than would have been standard even two years ago. Closing risk has gone from a conversation to a defining credit concern: lenders are reporting rescission rates of anywhere between 10% and 20% at closing, a staggering figure that reflects how much the market has moved since many of these purchase agreements were signed.

Ontario and Ottawa recently announced a significant expansion of the HST rebate on newly constructed homes. The program removes the full 13% HST on new homes valued up to one million dollars which is up to $130,000 in savings per buyer. It extends the same maximum relief to homes valued between $1 million to $1.5 million. Critically, this is no longer a first-time buyer program. For a one-year window, all buyers are eligible, regardless of whether they have previously owned a home. For developers, this is among the most meaningful demand-side policy moves in years. A buyer who signs a purchase agreement this spring on a sub-million-dollar unit faces a tax burden that has effectively just been eliminated for a year. The government’s own estimate puts incremental housing starts attributable to the measure at 8,000 per year in Ontario. Whether that holds up in practice will depend heavily on buyer confidence, financing conditions, and the broader economic backdrop but for product in the right price range in the right locations, this announcement deserves to be part of every presale conversation happening in Q2.

Inventory financing has tightened further. Spreads have continued to widen, and leverage has continued to decrease (relative to developer’s internal values), consistent with the trend we have been tracking since mid-2025. With re-sales slow and carrying costs elevated given the bond yield movement through the quarter, liquidity in this segment is increasingly selective.

Land financing remains scarce. Extensions are being granted in most cases, but lenders are requiring meaningful paydowns that reflect where values actually sit today, not where they were when the loan was originated.

Conclusion

Q1 2026 is a quarter defined more by what is shifting than by what has resolved. Bond yields moved quickly, execution timelines stretched, and sponsors who had been waiting for a more constructive environment found themselves re-underwriting deals mid-quarter. The CMHC pendulum has swung back toward insured construction, driven by declining rents and the approaching September energy efficiency deadline. The pre-sale and land markets remain effectively frozen. The HST relief legislation, represents the most meaningful demand-side policy signal for new construction in years. Through all of it, the deals getting done share the same characteristics they have for the past several quarters: in-place income, credible sponsorship, and structures underwritten to where the market actually is.

Sign up for our newsletter

.svg)

.svg)