.svg)

Q3 2025 Commercial Mortgage Market Update

After a relatively quiet summer, Q3 ended with a surge of activity following Labour Day. On September 17, the Bank of Canada (“BOC”) cut the overnight rate for the first time this year, lowering it to 2.50%. The move was attributed to weaker job numbers and slowing economic growth, though the BOC remained notably reserved on whether further cuts are forthcoming. South of the border, while President Trump pushed for an aggressive 100-basis-point reduction, Federal Reserve Chair Jerome Powell opted for a more measured 25-basis-point cut. Powell also signaled the possibility of two additional cuts before year-end 2025 should employment data continue to soften. Remarkably, this marks one of the rare occasions in history where the Fed has eased policy while the Dow sits at record highs.

Real Estate Challenges Continue

The Canadian real estate market remains under pressure, with headlines in both the commercial and multi-family sectors continuing to strike a cautious, if not outright pessimistic, tone. Uncertainty stemming from tariff threats, a pullback in overall investment, particularly from foreign sources, and a sharp slowdown in the condominium sector have all contributed to this subdued environment. While we have observed a modest uptick in acquisition activity, most participants would agree that attractive opportunities remain scarce in today’s market. Meanwhile, OSFI has publicly encouraged banks to pursue “smart” risk-taking in commercial credit, even suggesting potential adjustments to capital treatment by year-end which is a clear acknowledgement that future growth cannot rely on the residential sector alone.

Stat Can released their Q3 population estimates in late September, with a few figures that are wildly different than the trends seen in the past five years. For Canada overall, population growth YTD was seen at 77,000, a stark departure from nearly 770,000 added in 2024 and the nearly 1,000,000 in 2023. For Ontario, this is even more glaring, with a mere 2,710 people added, compared to 410,000 and 538,000 the two previous years. If trends continue, it will likely put further downward pressure on both housing prices and asking rents.

Lending Market Trends

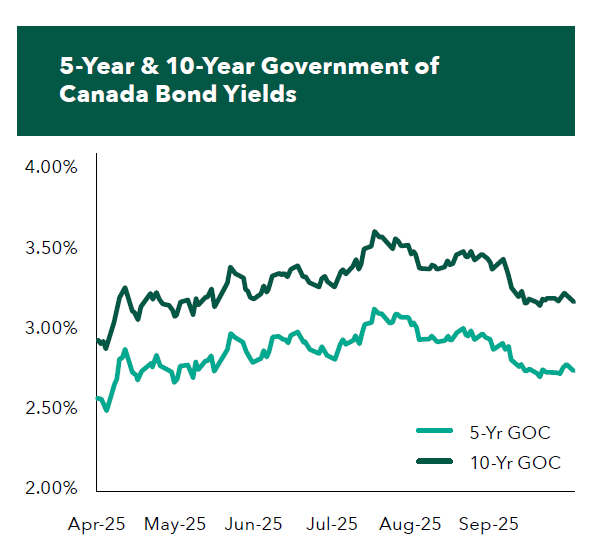

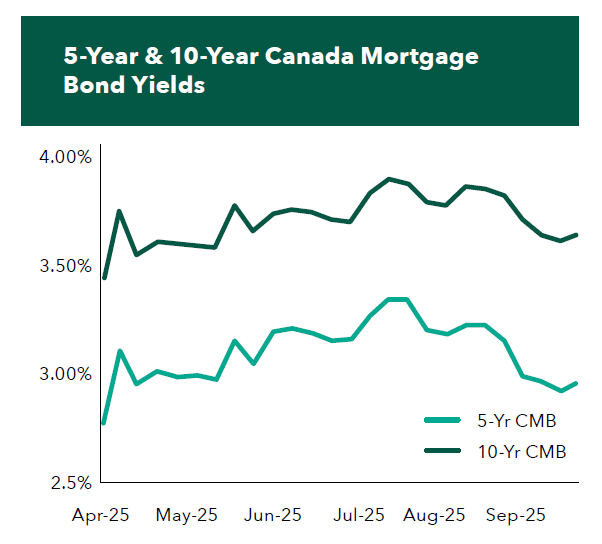

Lending spreads for income-producing properties have held steady compared to last quarter, with opportunities for AAA assets in core Canadian markets still commanding attractive spreads in the low to mid-100s. Encouragingly, with return-to-office mandates gaining traction, some lenders have begun to revisit the office sector, quoting new loans where this was previously a full-stop. Refinancing has also picked up as borrowers move to take advantage of declining bond yields. That said, transaction timelines continue to extend, as lenders across the board remain stretched as they balance workload from legacy “problem” files and new originations.

CMHC Update

Unsurprisingly, the multifamily asset class remains the product that lenders have the most appetite for, whether it be for insured or uninsured lending. CMHC backlogs remain high, with some underwriters becoming increasingly bureaucratic and looking for reasons to decline applications or post-approval amendments. Whether or not this is a directive from top CMHC brass to clear the logjam that is the current CMHC queue (approx. 2,300 applications), we caution Borrowers to have all their ducks in a row for their CMHC applications, especially in with respect to organizational structure and shareholder/limited partnership disclosure.

On a more constructive note, we have observed a handful of CMHC lenders offering mezzanine “top-up” financing for MLI Select construction loans facing rental achievement holdbacks. While typically limited to borrowers with strong sponsorship and capped at 85% loan-to-cost, this is an attractive option for Borrowers looking to limit equity in their construction projects.

Separately, on September 22, CMHC announced another rule change—this time targeting approved lenders and the annual CMHC loan allocations they are permitted to originate and fund. With nearly 100 approved lenders (though not all active), the current system has allowed active “aggregators” to exceed allocations by syndicating loan positions to less active players (mainly credit unions, smaller trust companies, and in some cases pension funds). That flexibility will end by April 2026.

In the near term, this change will likely push CMHC loan pricing higher, as demand exceeds the capped allocations of active lenders, and while nonactive lenders scramble to establish origination capabilities. Over the longer term, as these nonactive lenders lose their allocations, we anticipate that allocations will eventually shift toward the more active players, restoring balance to the market—though this rebalancing could take a year or more.

Condo Market Still Falling

Condo construction remains challenged, with demand plunging to 40-year lows. In August, CMHC reported a 16% month-over-month decline in national housing starts, led by pronounced weakness in multi-unit activity. The GTA market mirrored this trend, with new-home sales slipping further and reinforcing the demand reset that began last year.

That said, lender interest has not disappeared entirely. Well-located, “realistically” priced projects with credible cost-to-complete and in-place presale continue to attract financing—though these projects are increasingly rare. The bright spots: input-cost stability is increasing, slightly lower base rates, and better dialogue on clubbed senior/mezz structures to right-size equity. Deals are getting done; they just need to be built on today’s absorption, not 2021’s.

A further blow to investor sales comes from OSFI’s clarification on how lenders must treat income producing residential real estate. Under former guidance, lenders were able to count the same employment income and rental income used for Property A in order to obtain a mortgage to acquire Property B. Under new guidance, the income that was used to qualify for Property A can no longer be used at all for Property B. This will significantly limit “mom and pop” investors from purchasing multiple properties as the rules comes into effect in the first quarter of 2026.

Inventory Financing Tightening

Inventory loan activity has increased, but lenders remain highly selective, placing greater scrutiny on sponsorship strength, project location, and rent-to-sell fallback strategies. This caution was underscored by a headline-grabbing event in Oakville in September, when Greenpark opted to clear its remaining units in the mid-$600s psf, a move widely framed as a “rug pull” on surrounding resales and their existing buyers. Whatever the label, it is the kind of price discovery that makes inventory loan underwriting tougher in the short term and pushes lenders to haircut collateral values, shorten terms, and ask for more cash sweeps. Sponsors holding better-than-average units in A-locations can still find 60%–65% solutions with banks, trusts, and debt funds, but timelines have stretched and due diligence is more thorough.

Conclusion

Overall, the Q3 financing environment showed improvement over the first half of the year. The BOC has begun easing, the Fed has delivered its first cut, and bond curves remain calm. Industrial and necessity-retail term debt continues to be readily available. Multifamily construction remains financeable, provided today’s documentation standards and underwriting math are respected. Condo development is still achievable for disciplined sponsors with realistic pricing and genuine presales, while land financing increasingly requires defined milestones. Inventory loans remain an option, but the Oakville events serve as a reminder that approvals are won with data, not hope.

Looking ahead, the silver lining is that if inflation continues to ease, and another modest rate cut before year-end is possible. Until then, keep leverage sensible, lock when the numbers work, and move while lenders are still taking meetings.

Sign up for our newsletter

.svg)

.svg)